THE 2029 MUSIC INTELLIGENCE CRISIS

A Thought Exercise in Music Industry History, from the Future

What follows is a scenario, not a prediction.

I am modelling a future that neither side of the AI debate in our industry is properly considering. If you think AI is nonsense that will never touch real artists, this piece is for you. If you think the music industry is already dead and AI is the final nail, this piece is also for you.

Both positions are wrong, and the real danger lives in the space between them.

I wrote this as a speculative memo from the future, inspired by a piece from Citrini Research that imagined the broader economic fallout of AI.

This is my version for the music industry.

I wrote it because neither the dismissers nor the doomers are modelling the second-order effects. The crisis I describe below does not require AI to replace Beyonce. It does not require the death of all music. It requires something far more mundane: a slow, structural erosion of the economics that support the 99% of professionals who are not Beyonce.

This is The Black Hoody Industry Memo from March 2029.

Industry Memo

Both Sides Got It Wrong

The Black Hoody

March 21, 2026 March 30th, 2029

The IFPI released its Global Music Report this morning. Global recorded music revenues fell 11.4% year on year. It is the first annual decline since 2014 and the largest single year contraction since the depths of the piracy era.

Three years ago, the global recorded music industry was worth $31.7 billion and growing at 6.4% annually. Streaming subscribers had hit 837 million. The IFPI’s 2026 report celebrated an “eleventh year of consecutive growth.” Every region was up.

Three years. That is all it took.

There were two dominant views in 2026. The first, popular among established artists, successful managers, and veteran label executives, went something like this: “AI music is a gimmick. It has no soul. Real fans want real artists. This will blow over like every other tech fad.” The second, popular among indie artists, songwriters, and industry pessimists: “AI will replace all of us. The industry is finished. We are all going to be out of work.”

Camp 1 turned out to be right about the art. AI never replaced the great artists. It never wrote a song that moved a stadium to tears. It never built a fanbase through years of touring small rooms. The emotional connection between a human artist and a human audience remained irreplaceable in 2029, and it will remain irreplaceable for as long as music exists.

Camp 2 turned out to be right about the economics. The financial structures that supported the music industry were far more fragile than Camp 1 believed. The money that paid for artist development, that sustained managers, that funded festivals, that made sync licensing viable: that money was protected by the scarcity of the supply. And AI ended that scarcity.

The tragedy is that Camp 1’s confidence in the art blinded them to the economics. And Camp 2’s panic about the economics blinded them to the fact that the crisis was survivable, if the industry had acted in time.

Nobody acted in time.

The Scarcity That Held Everything Together

To understand what broke, you need to understand what was holding the music economy together in the first place.

It was not the quality of the music. There has always been far more quality music than any person could listen to. The music economy was held together by the cost of production. Recording a professional-sounding track required a studio, an engineer, a producer, musicians, mixing, mastering. It cost money and it took time. This acted as a natural filter. The economics of the industry were built on the assumption that producing music at a professional standard would always require meaningful human effort and capital.

AI removed that assumption.

In early 2026, the major labels were striking licensing deals with AI companies. Warner settled its lawsuit with Suno. Universal settled with Udio. Spotify announced plans for AI remix tools. Suno had hit 2 million paid subscribers and $300 million in annual recurring revenue by February 2026. Nearly 100 million people had used the platform.

The labels saw this and calculated their cut. They licensed their catalogues, collected upfront fees, and told shareholders that AI was a new revenue stream. What they failed to calculate was the cost of what that licensing unleashed.

How It Started

In late 2026, Suno shipped its V6 model. The audio quality crossed a threshold that the industry had been dreading but had convinced itself was years away.

A competent prompt writer could now generate a track in under 60 seconds that was, for the purposes of background listening, indistinguishable from a track made by a human in a studio. A workout playlist. A study session. Something to fall asleep to. The output lacked emotional depth. It had no artistic ambition. Camp 1 was right: this was not art.

But Camp 1 had made a fatal miscalculation. They assumed that because AI music was not art, it would not matter. They forgot that the vast majority of streams on Spotify are not art either. They are functional. Background noise for cooking, commuting, working, sleeping. The 50 million tracks on Spotify that nobody would notice if they were quietly replaced with something else.

Those tracks represented an enormous share of total streams. And the economics were straightforward: why would Spotify pay royalties on a playlist track when it could generate a functionally equivalent one for a fraction of a cent?

SPOTIFY Q1 2027: LAUNCHES “AMBIENT” AND “FOCUS” PLAYLISTS FEATURING AI-GENERATED MUSIC; REPORTS 30% REDUCTION IN PER-STREAM ROYALTY COSTS FOR FUNCTIONAL MUSIC CATEGORIES | Music Business Worldwide, April 2027

Nobody was surprised when it happened. Spotify had been building towards this for years. Liz Pelly’s reporting had already documented how the platform relied on cheap background music to pad playlists and reduce its royalty obligations. AI made that strategy infinitely scalable.

Camp 2 saw this headline and said “told you so.” Camp 1 shrugged and said “that is not real music anyway, it does not affect us.”

Both were wrong about what happened next.

Streaming Was Finally Working. AI Broke It.

Streaming was working. That is what makes this so painful to write about.

As I wrote in The Black Hoody in 2024, there is more money in music now than there has ever been in human history.

The global music copyright market hit $45.5 billion in 2023, 38% larger than the entire global cinema industry. Recorded music revenues reached $31.7 billion in 2025. Paid streaming subscribers passed 837 million.

Thousands of artists nobody has heard of were making real livings. An independent artist with 10 million monthly Spotify streams was generating roughly $390,000 net annual revenue from streaming alone. Artists like BBNO$, Marlon Craft, Brother Ali: no household fame, real income. Before the streaming era, that was not possible. The long tail of music was finally making money.

The people who said streaming does not pay were, broadly, wrong. The people who said there was more opportunity than ever were, broadly, right.

AI is threatening to undo all of that progress.

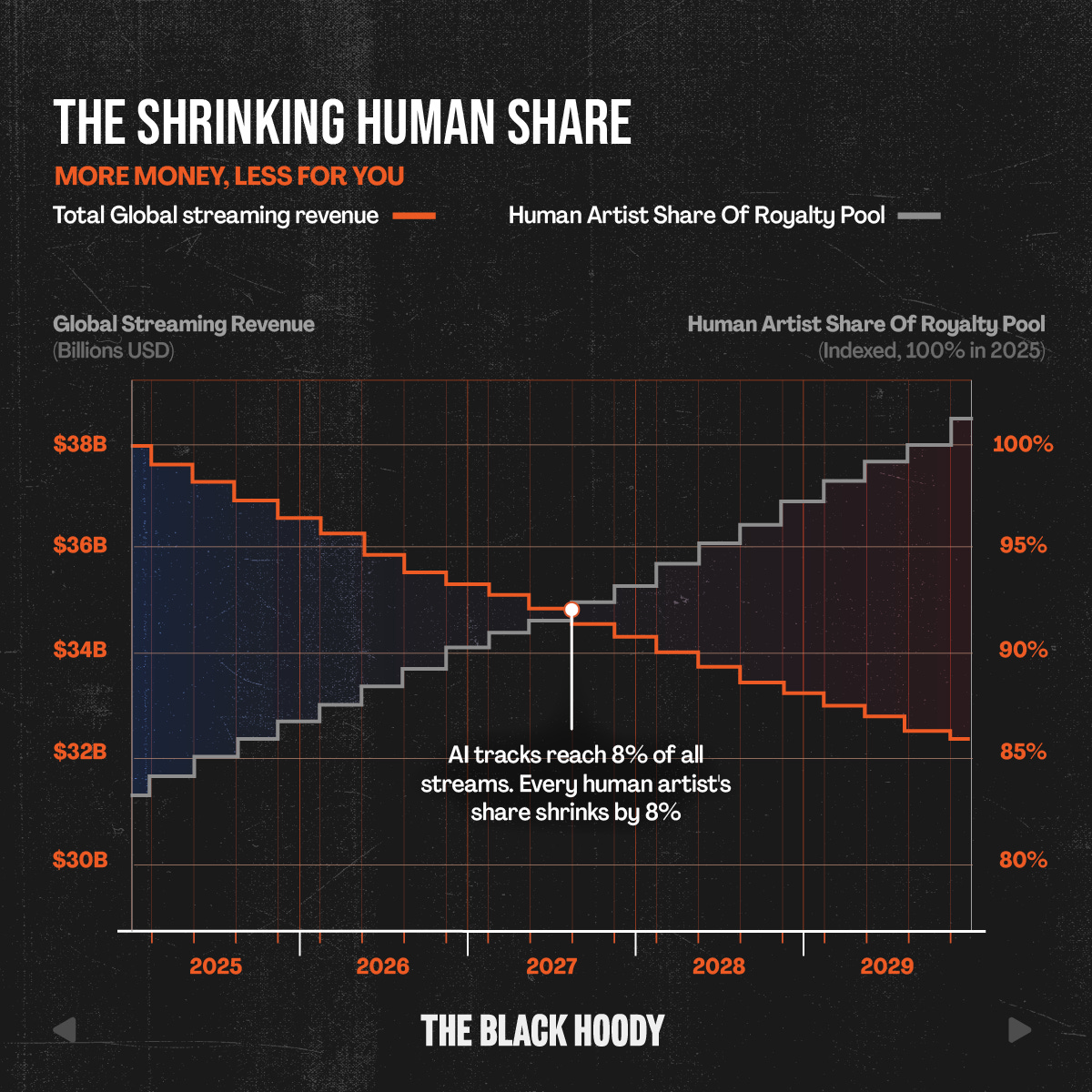

When AI-generated tracks grew to an estimated 8% of total streams across all major platforms by Q3 2027, every human artist’s share of the pro-rata pool shrank by 8%. This had nothing to do with whether their fans listened to AI music. The pool is shared. The dilution is automatic.

Eight percent of a $22 billion streaming market is $1.76 billion in annual revenue redirected away from human creators. The labels were collecting licensing fees from the AI companies, but those fees were a fraction of what the dilution was costing them.

ASCAP REPORTS 4.2% DECLINE IN TOTAL DISTRIBUTIONS FOR FY2028; CITES “STRUCTURAL CHANGES IN THE STREAMING ROYALTY ENVIRONMENT” AND “INCREASED VOLUME OF NON-HUMAN-ORIGINATED WORKS” | Variety, February 2028

The independent artist who was making $390,000 a year in 2025 was now making $310,000. Still a living, yes. But the artist below them, the one making $80,000, was now making $64,000. And the one below them, the songwriter making $30,000, was now at $24,000. The margins were already thin. AI did not break a system that was already broken. It broke a system that was finally starting to work.

That is what made this crisis so perverse. The industry had spent a decade clawing back from piracy. Streaming had created a genuine middle class of working musicians for the first time in history. AI attacked the model that had just been fixed.

Camp 1 did not notice because Camp 1’s artists were doing fine. The top 1% always is. Camp 2 had spent so long saying streaming was broken that when AI actually broke it, nobody listened to them.

The Pipeline Collapse

The crisis in artist management was not about managers being replaced by AI. It was about the destruction of the pipeline that produces skilled managers in the first place.

I have managed artists for over 17 years. The fundamental business model has never changed: the manager works for free until the artist makes money, then takes a commission. The entire profession is a bet that the artist will eventually generate enough income to make the years of unpaid labour worthwhile.

The way you learn management is by doing it. You start with a young, unknown artist. You make mistakes. You learn how to negotiate, how to read a contract, how to build a campaign, how to manage an artist’s expectations when reality does not match their ambitions. That education takes years, and it only works if the artist you are managing generates enough income to keep you in the game while you learn.

When mid-tier artist incomes dropped 20-30% due to royalty pool dilution and the sync collapse, the emerging artists below them were hit harder. A new artist who might have generated $40,000 a year in streaming income (enough, barely, for their manager to survive on a 20% commission of $8,000 while building towards something bigger) was now generating $28,000. The manager’s cut dropped to $5,600. Brutal.

MMF (MUSIC MANAGERS FORUM) UK: MEMBERSHIP DECLINES 18% IN 2028; SURVEY FINDS 41% OF MANAGERS UNDER 35 HAVE LEFT THE PROFESSION IN THE PAST 24 MONTHS | The Music Network, September 2028

The same dynamic played out across every junior role in the ecosystem. Labels cut entry-level A&R positions and replaced them with AI-powered analytics dashboards. Publicists were replaced by automated campaign tools. Junior marketing coordinators were replaced by generative content platforms. Each individual cut was rational. Collectively, they eliminated the training ground where the next generation of music executives would have learned their craft.

The industry was eating its seed corn. The 25-year-old A&R assistant who got cut in 2027 was the person who, by 2035, would have had the ears and relationships to sign the next generation of artists. That person now works in SaaS sales. They are never coming back.

Artist management industry already had a real shortage of talented managers because the stress-to-remuneration ratio was so punishing. AI made the financial equation worse at the exact moment it was eliminating the junior roles that train the next generation. The profession was losing experienced operators at the top and cutting off new entrants at the bottom simultaneously.

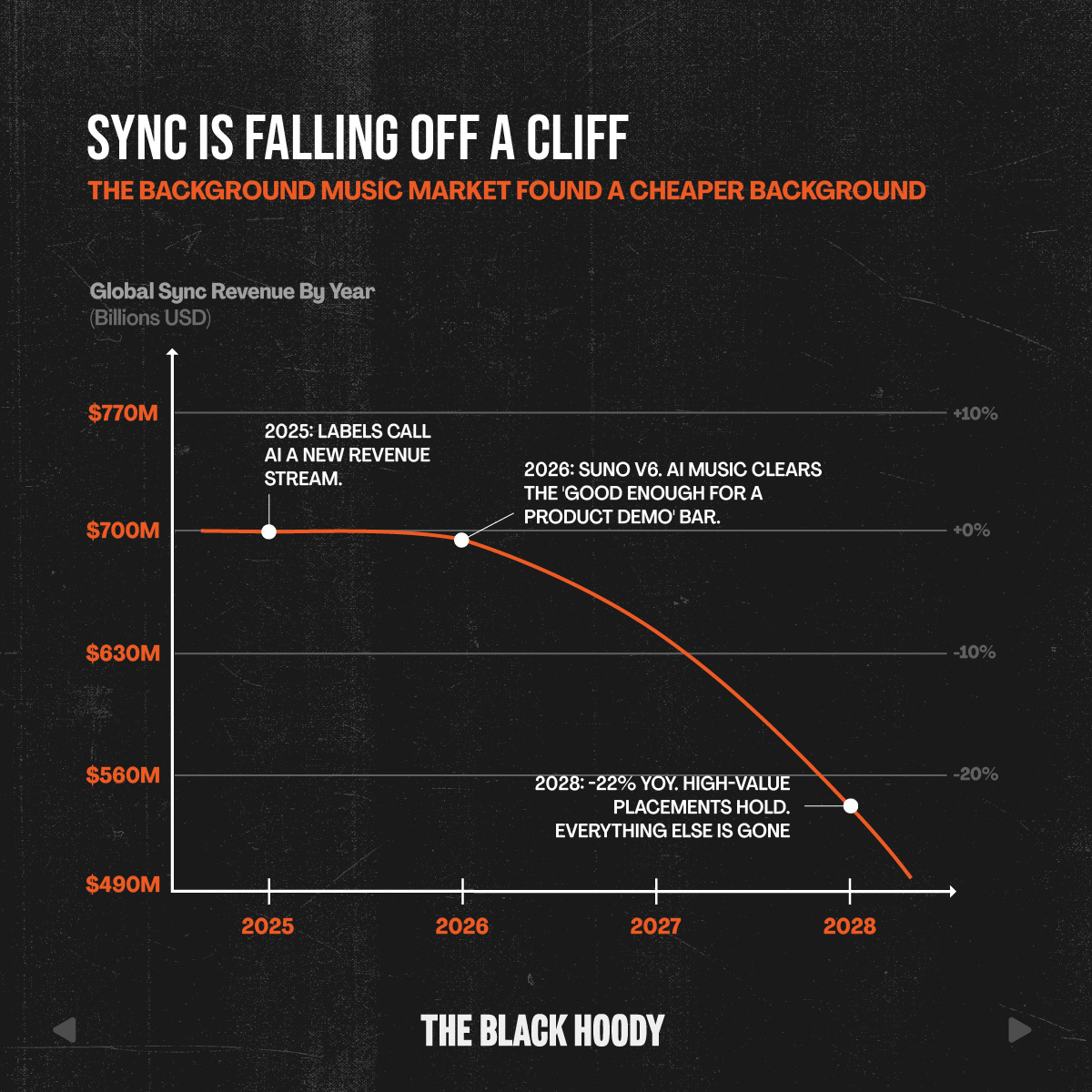

The Sync Collapse

For a decade, sync licensing had been the financial backbone of the middle class musician. A song placed in a TV show or a commercial could generate more income than years of streaming.

AI gutted it in 18 months.

By early 2028, production companies and ad agencies discovered what every budget-conscious content creator already knew: AI tools could generate purpose-built music for a specific scene in seconds, for essentially zero marginal cost.

A music supervisor who previously had to search through catalogues, negotiate licensing fees, and clear rights across multiple parties could now type “upbeat indie rock, female vocal, themes of freedom, 90 seconds” into Suno and get something fantastic before their coffee went cold.

The output lacked the emotional complexity of a great sync placement. For 80% of use cases, it did not need to have it. Most sync placements are background music in a reality show or a product demo. The kind of thing nobody Shazams.

Global sync revenues had already declined 2% in 2025, from $700 million to $641 million. By 2028, the decline accelerated to 22% year on year. High value placements in major films and premium television held up. Everything else cratered.

The $5,000 web content placements. The $2,000 library music licences. The small deals that kept managers’ lights on and songwriters housed. Gone.

The Catalogue Reckoning

We already had a preview of what happens when music catalogue valuations do not hold up. Hipgnosis Songs Fund spent approximately $2.2 billion acquiring catalogues between 2018 and 2021, lost more than half its market value, and was ultimately sold to Blackstone for $1.6 billion in July 2024. Founder Merck Mercuriadis stepped down.

The fund was rebranded as Recognition Music Group in 2025 before Sony Music Publishing acquired the Hipgnosis Songs Group subsidiary. The “future of music publishing,” as it was once called, collapsed under the weight of overspending and mismanagement before AI had even become a serious factor.

Now imagine what happens when AI becomes a serious factor.

Between 2020 and 2025, dozens of private equity firms followed the same thesis that Hipgnosis had pioneered: buy music catalogues, underwrite them on the assumption that streaming revenues would grow indefinitely, and collect passive income forever. Primary Wave, Concord, and funds backed by KKR, Apollo, and Blackstone itself poured billions into song rights.

The value of a music catalogue is a function of its future royalty income, discounted to the present. When per-stream rates fell and the royalty pool contracted, the projected future income of every catalogue on the market declined with it.

MAJOR CATALOGUE FUND WRITES DOWN NET ASSET VALUE 19.3%; BOARD CITES “MATERIAL CHANGE IN LONG-TERM ROYALTY GROWTH ASSUMPTIONS” AND “STRUCTURAL HEADWINDS FROM AI-GENERATED CONTENT” | Financial Times, November 2028

The funds that had paid 25-30x net publisher share multiples were now looking at catalogues worth 14-16x. Falling. The institutional investors who had been told music was a safe, uncorrelated asset class started asking uncomfortable questions.

Every dollar Spotify saved by replacing catalogue tracks with AI-generated alternatives came directly out of the royalty streams these funds depended on. Hipgnosis had been a cautionary tale about operational mismanagement. AI made the cautionary tale structural.

The Label Paradox

Through 2027, Universal, Warner, and Sony maintained their revenue growth by cutting costs and leaning into the disruption.

They cut A&R staff. Why pay a team of 20 to find new artists when AI analytics tools could surface emerging talent from social data in hours? Marketing teams followed. Then admin headcount. Then regional offices.

Each label’s individual response was rational. The collective result was something else entirely.

Universal’s Q2 2028 earnings call reported a 14% reduction in global headcount alongside record operating margins. The analysts loved it. The stock rallied. The people who got fired were the ones who spent years learning how artists actually break: the people who understood why one campaign works and another does not, who could read an audience’s energy at a live show and know whether an artist was ready, who had the instinct to invest in an act that no algorithm would have flagged. These skills take a decade to develop. They cannot be replaced by a dashboard.

The labels had been struggling to break new artists for years. Social media had already disrupted the old playbook. The answer was supposed to be innovation: new methods, new platforms, new strategies for connecting artists with audiences. Instead, the labels responded to AI disruption by cutting the humans who were supposed to figure out the new playbook.

UNIVERSAL MUSIC GROUP: RESTRUCTURES DOMESTIC OPERATIONS IN KEY MARKETS; A&R TEAMS REDUCED BY 40-60%; “AI-ASSISTED ARTIST DEVELOPMENT” TOOLS TO SUPPLEMENT REDUCED STAFF | The Music Network, Q3 2028

The labels were saving money by firing the people who made them money. The savings went into licensing more AI tools. Which accelerated the disruption. Which required more cost cutting.

A feedback loop with no natural brake.

The Live Music Inversion

The consensus view in 2026 was that live music would be the safe harbour. AI could not replicate the experience of seeing an artist perform in a room. This was Camp 1’s strongest argument, and on its face, it was correct.

What actually happened was stranger than either camp predicted. Live music did not collapse. It inverted.

The artists who could perform, the ones who were electric on stage, who could hold a room, who made people feel something in person, those artists started making more money than ever. Many of them had never had a big recorded music profile. They were session musicians, jazz players, local heroes who packed out small venues every weekend. In a world where recorded music income was shrinking, the ability to walk into a room and earn money that night became the most valuable skill in the industry.

This was not the win Camp 1 imagined. It was a regression.

The economics of live performance do not scale the way recorded music does. A recorded hit can generate millions of dollars while the artist sleeps. A live performer has to show up, every night, in a physical room, to earn. There is a hard ceiling on how many shows a person can play in a year, how many cities they can travel to, how much their body can take.

The artists who had previously built their income on recorded music found that revenue stream shrinking. They were forced to tour more, play more shows, work harder physically to maintain the same income. The freedom that recorded music royalties had provided, the ability to take time off, to write, to be creative without performing, was disappearing.

Now consider the counter-argument. Live music can scale. Taylor Swift sold out multiple stadium runs across continents. Coldplay played to millions. At the very top, live music is an enormously scalable business.

But how did Swift and Coldplay get to stadium level? Through decades of recorded music dominance. Billions of streams. Global radio play. Sync placements in every market. The kind of cultural saturation that only comes from having your music embedded in the daily listening habits of hundreds of millions of people. You do not sell out a stadium because you are a great performer. Plenty of great performers play to 200 people on a Tuesday night. You sell out a stadium because your recorded music made you famous in every country on earth.

That is the pipeline AI broke.

The session musicians and local heroes making more money in the inversion will never reach stadium level. They will never have the global profile that recorded music dominance creates, because the recorded music economy that builds those profiles is contracting. They will earn well at venue scale. They will work hard for it. And they will hit a ceiling that previous generations of artists could break through.

The mid-tier touring artist was squeezed from both directions. The one playing 500 to 1,500 capacity rooms depended on streaming income and sync revenue to subsidise their touring costs. Without that subsidy, the economics of getting in a van and crossing a country stopped making sense. And the path from 1,500-cap rooms to 15,000-cap arenas, which required a recorded music breakout to build the audience, was narrowing as labels cut investment in artist development.

The festivals that depended on mid-tier artists for their lineups were hit next. Major festivals around the world had already been folding or being cancelled for years due to rising costs and weakening lineups. The festivals that survived into 2027 found their booking options shrinking as fewer artists could afford to tour.

Live music split into two economies: global superstars who had built their profiles in the pre-AI era, and local performers earning a living one room at a time. The vast middle ground, the 500-cap to 5,000-cap circuit that had been the backbone of artist development for decades, was hollowing out. And the mechanism that created new stadium acts, recorded music dominance, was the very thing AI was eroding.

What Both Camps Missed

The music industry’s displacement spiral ran like this:

AI music tools improved. Streaming platforms integrated AI-generated content. The royalty pool diluted. Artist income fell. Managers and support staff left the profession. Artist development slowed. Labels cut headcount and redirected savings to AI tools. AI music tools improved.

Each link in the chain was a rational response to the link before it. No individual decision was wrong. The system was destroying itself.

Camp 1 watched each link break and said “that does not affect my artist.” They were correct about each individual link. They missed the chain. By the time the effects reached their artist’s touring support, their artist’s sync income, their artist’s label investment, it was too late.

Camp 2 watched each link break and said “we’re all finished.” They were wrong because the crisis was never about AI replacing music. It was about AI replacing the economics that supported the ecosystem around the music. Those economics could have been restructured. The industry had time in 2026 to ring-fence human-created royalty pools, to create separate streaming tiers, to build new economic structures around verified human artistry. The doomers’ fatalism gave the industry permission to do nothing.

The dismissers did not act because they did not believe it was necessary. The doomers did not act because they did not believe it was possible.

The Question

At the core of this crisis was a question that the music industry never honestly confronted: what is the value of human-made music in a world where machines can make infinite music for free?

For the entirety of recorded music history, human creativity was the scarce input. Capital was necessary. Distribution was necessary. Without a human being writing a song, recording a performance, and connecting with an audience, none of it mattered.

AI made creativity abundant. The output was not better. It was not more emotionally resonant. It was just everywhere, in quantities that overwhelmed the economic structures built on the assumption of scarcity.

Piracy, the last existential threat, had a clear message: “Your music is worth something, but I refuse to pay for it.” The industry responded with a better distribution model and survived.

AI’s message was different: “Your music might not be worth paying for, because I can make something close enough for free.”

The first threat required better distribution. The second required a fundamental revaluation of what human-made music means to the world. The industry needed to build economic structures that protect and reward human creativity specifically because it is human.

Whether we build those structures in time is the only question that matters.

But you are not reading this in March 2029. You are reading this in March 2026.

The global recorded music industry just celebrated its eleventh consecutive year of growth. Revenues hit $31.7 billion. Streaming subscribers reached 837 million. The IFPI report is full of optimism.

Suno has 2 million paid subscribers and $300 million in annual revenue. Nearly 100 million people have used the platform. Deezer is receiving over 60,000 fully AI-generated tracks per day. Spotify deleted 75 million spammy tracks last year alone.

The labels are licensing. The AI companies are growing. The artists are split between “it won’t affect us” and “it’s already over.”

Both are wrong. And neither is doing anything about it.

Luke Girgis has written one of the sharpest analyses of what AI is doing to the music industry’s economics that I’ve read. The scarcity argument holds up. The displacement spiral is real.

The part about the pipeline collapsing, destroying the training ground for the next generation of music professionals, is the most important thing in the piece, and he’s right to name it. But the entire scenario he maps out rests on an assumption so deep he never questions it: that creatives are passive.

That artists sit inside whatever economic structure the industry builds around them and wait to see if it survives. History doesn’t support that. When sheet music publishing collapsed, composers found radio.

When piracy gutted the album economy, musicians found touring, merch, Bandcamp, Patreon. Every supposed extinction event in music turned out to be a forced evolution. The ones who called it death were the ones too attached to the previous form to see the next one taking shape.

This isn’t an AI problem. It’s an imagination problem. The creatives genuinely at risk in any version of 2029 aren’t the ones technology replaced. They’re the ones who spent three years waiting for AI to go away, still trying to optimise a model that had already moved.

The assumption that the future will look like the past, that success still means streaming numbers and sync deals and label investment, is the real crisis underneath the one Luke is describing. In a world of infinite synthetic content, the rarest thing in the room isn’t a great-sounding track. It’s a documented human story. A mythology.

A community built around something real. AI can generate music. It cannot generate thirty years of cultural authority, a specific city, a specific moment, a specific journey that people witnessed and remember.

The door Luke says is closing is not the only door in the building. The middle-class musician he mourns was always one platform decision away from losing everything, because the income was never really theirs to own.

What his 2029 scenario actually reveals, if you read it as a signal rather than a sentence, is where human value relocates when synthetic content becomes abundant. The artists building direct relationships with their audience, converting listeners into members, turning cultural authority into something a community wants to fund and be part of, those artists aren’t in the royalty pool AI is diluting.

They’re running a different economy entirely, one that gets stronger as synthetic noise floods the market, because belonging and authenticity become the scarcest things available. The building isn’t burning.

The map is wrong. The creatives who’ve always found the next form will find it again.

Excellent stuff LG.